A buyer gets the appraisal back at value and assumes the house is fine. Then the inspection report shows roof leaks, unsafe wiring, and foundation movement. That disconnect is exactly why understanding home inspection versus appraisal differences matters. These are not competing services, and one does not replace the other.

For buyers, sellers, and agents, confusion usually starts because both happen around the same time in a real estate transaction. Both involve a professional visiting the property. Both can affect whether a deal moves forward. But they answer very different questions, and mixing them up can lead to expensive assumptions.

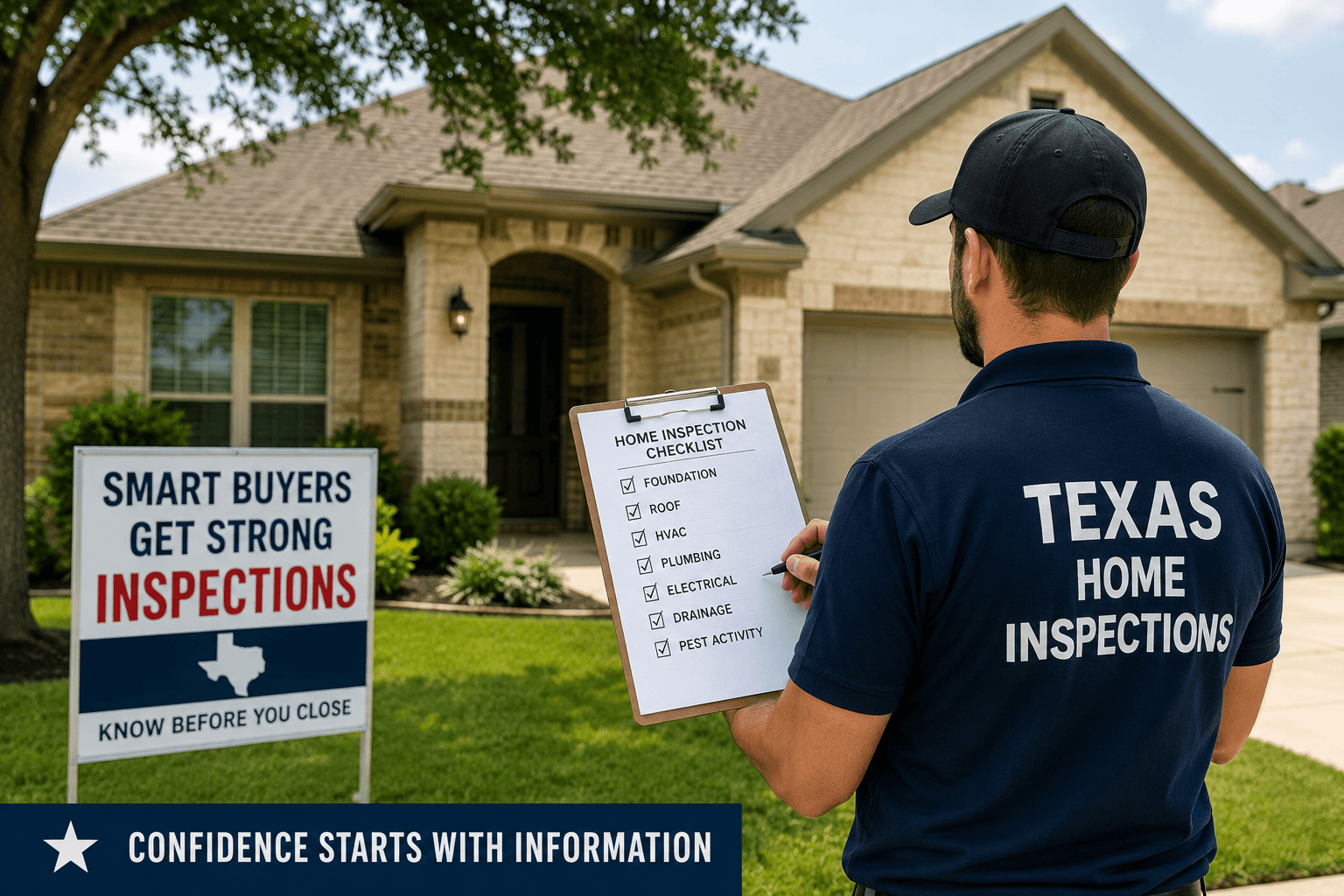

What an inspection is meant to tell you

A home inspection is about condition. The inspector evaluates the visible and accessible parts of the property to identify material defects, safety concerns, and systems that may be near the end of their service life. The goal is not to predict every future issue or tear the house apart. The goal is to give you a clear, factual picture of what you are buying.

That typically includes the roof, attic, structure, foundation, plumbing, electrical, HVAC, windows, doors, appliances, drainage, and more. In Texas Hill Country properties, that can also mean paying close attention to grading, moisture movement, exterior wear from heat and storms, and signs that a pier-and-beam or slab foundation may be shifting.

An inspection helps a buyer answer practical questions. Is the electrical panel safe? Is the air conditioner cooling properly? Are there active leaks, drainage problems, or structural cracks that deserve further evaluation? What repairs should be addressed soon, and what may become a budget issue later?

Just as important, a good inspection report should explain findings in a way that supports decisions without creating unnecessary panic. Not every defect is a deal breaker. Some are maintenance items. Some are negotiation points. Some deserve a specialist. Context matters.

What an appraisal is meant to tell you

An appraisal is about value. The appraiser is usually working for the lender to determine whether the property supports the loan amount. In simple terms, the lender wants to know whether the home is worth what the buyer has agreed to pay.

To do that, the appraiser looks at market data, recent comparable sales, location, square footage, condition, features, and overall appeal. The appraiser may note obvious condition issues, especially if they affect value or loan eligibility, but the appraisal is not a detailed defect investigation.

That distinction matters. An appraiser might observe that a home appears average for the neighborhood and assign a value that satisfies the lender, even if the property has aging HVAC equipment, a leaking roof, or plumbing problems hidden behind walls. The appraisal can support the price while telling you very little about repair risk.

Home inspection versus appraisal differences that affect your decision

The clearest way to understand home inspection versus appraisal differences is to look at purpose, client, and outcome.

The inspection serves the buyer, even when an agent coordinates it. Its outcome is a condition report that helps the buyer understand defects, maintenance needs, and possible repair costs. The appraisal serves the lender first. Its outcome is a value opinion used to support financing.

The inspection is usually far more detailed about the house itself. The appraiser is not testing outlets, examining the attic in the same way, evaluating roof installation quality, or checking whether the water heater is back-drafting. An inspector is not determining market value or comparing recent neighborhood sales.

Timing can overlap, but the decision each report informs is different. The inspection helps you decide whether the property is acceptable in its current condition and whether to negotiate repairs or credits. The appraisal helps determine whether the bank will lend based on the agreed purchase price.

Why a good appraisal does not mean a good house

This is one of the most common misunderstandings in residential real estate. Buyers hear that the home appraised and feel reassured. From a financing standpoint, that may be good news. From a condition standpoint, it means very little.

A house can appraise at full value and still need major work. If the market is strong, comparable sales may support the price despite deferred maintenance. Cosmetic updates can also influence perception while masking more expensive concerns. Fresh paint and new flooring do not tell you whether the foundation is moving or the electrical system has unsafe conditions.

That is why condition and value should be treated as separate issues. A property may be worth the contract price and still be the wrong purchase for your budget if repairs are substantial.

Why an inspection cannot tell you market value

The reverse is also true. A thorough inspection may uncover defects, but that does not automatically tell you what the property should be worth. Real estate value depends on location, inventory, buyer demand, lot size, upgrades, and comparable sales. A home with needed repairs may still command a strong price in a tight market.

An inspection gives you leverage and clarity, not a formal valuation. In practice, buyers often use the inspection findings to request repairs, ask for a credit, renegotiate price, or walk away if contract terms allow. But the amount of any concession depends on market conditions and the seller’s position, not just the existence of defects.

Who orders each service and who pays

In most transactions, the buyer orders the inspection and pays for it directly. That keeps the purpose clear. The buyer needs independent information about the property’s condition before moving forward.

The appraisal is usually ordered through the lender as part of the financing process, and the buyer typically pays for it as part of closing costs. Even though the buyer pays, the appraiser’s role is tied to the lender’s underwriting requirements.

This difference in client relationship helps explain why the reports are not interchangeable. One is due diligence for the buyer. The other is risk management for the loan.

What each report can trigger in a transaction

An inspection report can trigger repair requests, price negotiations, specialist evaluations, or a decision to terminate during the option period. If the report identifies roof damage, unsafe wiring, foundation concerns, or failing HVAC equipment, those findings may materially affect the buyer’s willingness to proceed.

An appraisal can trigger a different kind of problem. If the appraised value comes in lower than the contract price, the buyer and seller may need to renegotiate, the buyer may bring more cash to closing, or the deal may fall apart if no agreement is reached.

Sometimes the two reports intersect. For example, if an inspection identifies major condition issues, those concerns may influence negotiations before closing. If an appraiser also flags obvious deferred maintenance, that may complicate financing for certain loan types. But the reports still serve separate functions.

Which one matters more?

It depends on the question you are asking.

If you want to know whether the property is priced appropriately for the lender, the appraisal matters more. If you want to know whether the property has hidden defects that could cost thousands after closing, the inspection matters more.

For most buyers, especially first-time buyers or anyone watching their budget closely, the inspection is the more practical tool for avoiding unpleasant surprises. A low appraisal can disrupt financing, but a missed structural issue or major water intrusion problem can affect your finances long after closing.

That is also why experienced agents usually encourage buyers not to treat the inspection as a formality. It is one of the few moments in the transaction when you get a clearer view of what you are actually taking ownership of.

A practical example for Texas buyers

Imagine a home in the Hill Country with attractive updates and a sales price supported by nearby comps. The appraisal comes in at contract value. From the lender’s perspective, the file looks fine.

Then the inspection finds active roof leakage near a chimney flashing detail, double-tapped breakers in the electrical panel, poor drainage toward the foundation, and an HVAC system nearing failure. None of that necessarily prevents the home from appraising. But it absolutely affects the buyer’s risk, repair planning, and negotiation strategy.

That is where a thorough inspection earns its value. Clear findings, delivered promptly and explained without drama, help buyers decide whether to request repairs, budget for replacements, or step back before a costly mistake becomes theirs.

If you remember one thing, make it this: the appraisal tells the bank what the property may be worth today, while the inspection helps you understand what the property may cost you tomorrow. A calm, fact-based inspection gives you room to make that decision with confidence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}